Bank of Thailand: Economic and Monetary Conditions for July 2025

- The Thai economy softened from the previous month driven by a slowdown in the service sector and manufacturing production due to temporary factors, despite a rise in merchandise exports.

- Revenue from foreign tourism declined, reflecting reduced spending per trip amid promotional campaigns aimed at boosting visitor numbers. Meanwhile, total arrivals edged up slightly, supported by an increase in Chinese tourist arrivals.

- Manufacturing production declined due to temporary factors, including refinery maintenance and short-term halts in automobile production for process adjustments. Excluding these disruptions, industrial production improved.

- Merchandise exports increased, led by strong growth in exports of electronics and appliances, with continued growth in shipments to the U.S.

- Employment conditions remained broadly stable, though rising unemployment claimants relative to the number of insured workers warrants close monitoring.

- Key issues to monitor include: 1) the impact of U.S. trade policies, 2) the performance of the tourism sector, 3) developments at the Thai–Cambodian border and their effects.

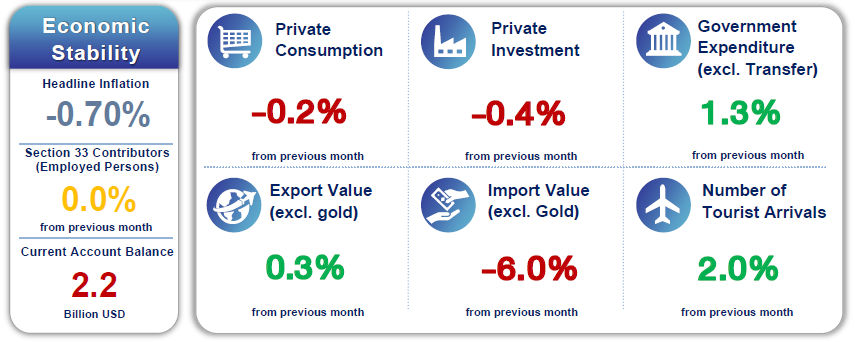

The Thai economy softened in July compared to the previous month, as activity in the service sector declined, due to weaker domestic and foreign tourism, reflected in lower tourism revenue. Manufacturing production also fell, driven by temporary factors such as refinery maintenance and short-term halts in automobile production for process adjustments. However, excluding these disruptions, industrial production improved, supported by strong merchandise exports. Private investment declined, primarily due to reduced spending on machinery and equipment. Meanwhile, private consumption remained broadly stable, but continued to face headwinds from weakening consumer confidence. Government expenditure expanded, driven by higher current spending from central government and increased state enterprise investment.

On the economic stability front, headline inflation turned more negative, driven by falling fresh food prices—particularly fruit and meat— and a further decline in energy inflation, in line with domestic and global oil prices. Core inflation moderated, reflecting high base effects from last year’s processed food prices and lower personal care product prices following promotional campaigns. The current account surplus narrowed slightly, mainly due to a smaller trade surplus. Employment conditions remained stable, though the rising share of unemployment claimants relative to insured workers warrants close monitoring.